Software M&A Deals in Challenging Markets

Covid-19 has had a dramatic impact on the overall markets and especially the venture capital and M&A markets. And while the market has bounced back significantly from recent lows, many clients are asking what this means for the private markets like M&A and raising VC capital. As such, we keep getting questions from various software companies on what is the best course in these challenging markets.

The extent of the challenging M&A market can be seen clearly in Figure 1 below. This shows a dramatic drop-off in both the number of transactions and the $ volume. While early Feb was elevated from typical weekly averages, the average weekly deal count in 2019 was still 30, way above what we have seen in recent weeks.

Figure 1 - North American Software M&A Deals by Week

Source: Pitchbook.

One other trend we talked about in a recent social media post was how PE money has quickly dried up. We’ve talked to many of the largest firms and just as many mid-market PE firms over the last several weeks and it has become noticeable how quickly they have shelved deals and stopped looking at new ones. Many are concerned about overpaying in an unpredictable market and are therefore paid to wait. This is especially a problem in a market where PE money has become increasingly important – see the chart below for the percentage of software deals made up by PE firms – which has steadily been growing over the last 5 years.

Figure 2 - North American Software M&A Deals by Buyer Type

Source: Pitchbook.

Unfortunately, the same is true for strategics. Over the last few weeks we’ve also talked to a lot of Fortune 500 and other strategics that used to be very active on the M&A front. Given their existing businesses are likely feeling the impact of a slowing economy, most have also put M&A on hold until they have more clarity on the broader macro market and their own business performance. The exception is the software consolidators that are still active but never really got to the elevated software multiples we have seen the last few years.

Where the PE firms have said they will continue to spend time is on the add-on acquisitions. Large acquisitions in a new area are usually called platform investments – one that PE firms grow both organically (by installing best practices) and inorganically – by conducting acquisitions of other smaller but similar companies (an add-on). So add-ons will likely continue but PE firms will be more price-sensitive as they look to use these acquisitions as a path to reducing their overall blended multiple (i.e. they pay >5x for a platform and 3-4x for an add-on – buying down the blended multiple across the whole combined business).

So, what does this all mean for software M&A deals? Well, it obviously means buyers are being a lot more selective. As such, the typical auction approach to selling a company likely won’t work and any sales happening in this market are truly strategic - either as an add-on acquisition for a PE firm or as a tuck-in acquisition for a larger strategic entity.

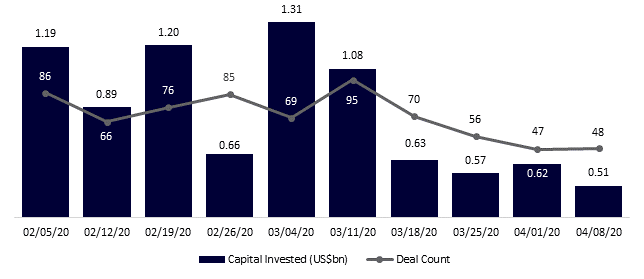

However, where we do see a pick-up in activity is distressed sales and mergers. Lots of companies out there either don’t have the capital cushion to weather a protracted market down-turn or were growth companies that are going to struggle to find additional VC money in a tight VC market. The drop-off in VC activity has already begun as can be seen by the chart below – and 2020 was already off by a lot from the 2019 weekly average deal count of 116!

Figure 3 - North American Software VC Deals by Week

Source: Pitchbook.

So, if you’re a software company looking to sell, if you can wait, we would suggest you do. If not, then the most viable path to success might be a merger with a similar-sized competitor or complimentary software company. But act quickly - mergers in these types of markets are very much like a game of musical chairs – the obvious merger candidates get snapped up quickly!

About Sampford Advisors

Sampford Advisors is a boutique investment bank exclusively focused on mid-market mergers and acquisitions (M&A) for technology, media and telecom (TMT) companies. We have offices in Toronto, Ottawa and the US and have done more mid-market tech M&A transactions than any other adviser.