Growth of Private Equity and Its Focus on Software

The amount of capital that has been flowing into private equity investments over the course of the past decade has been a well observed trend. This growth in the private equity industry can be at least partially explained by the recovery years following the financial crisis, with increasing numbers of investors looking to deploy capital in alternative investments. While the number of North American funds raising capital has remained relatively flat since 2013, the amount of capital raised annually has nearly doubled over that same time period. This growth in capital raised but not fund count indicates that private equity firms are raising increasingly larger funds. Larger fund sizes are likely a symptom of the rising competition for a limited number of assets or acquisition targets which is forcing firms to pay higher valuations.

Source: Pitchbook.

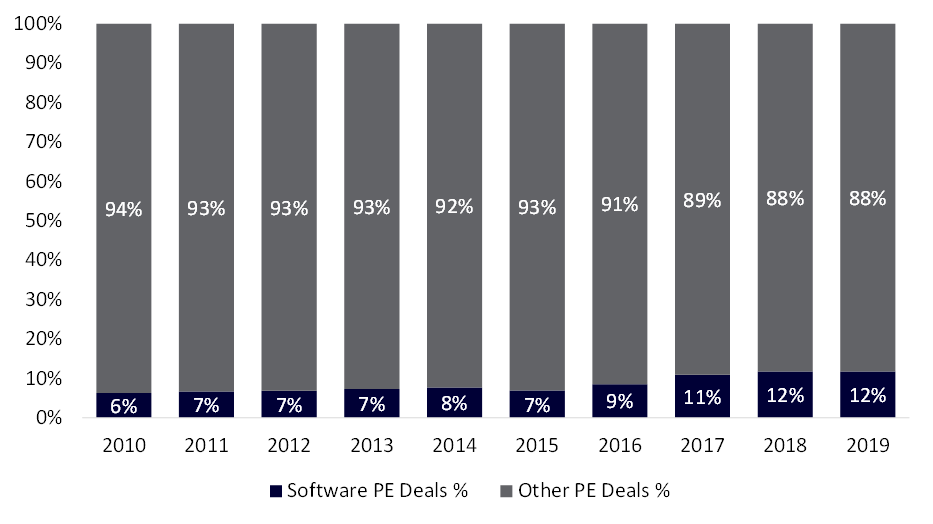

One sector where private equity has become more active over the past decade has been Software. Private equity’s share of total software M&A deals has nearly doubled from 2010 to 2019 and now accounts for over a third of all Software deals. Following an almost identical trend, Software as a % of total private equity deals has also doubled in the same timeframe. These two trends confirm that an increasing portion of the substantial capital that is flowing into private equity is being funneled directly into Software investments.

Source: Pitchbook.

Source: Pitchbook.

Private Equity vs. Strategic Software Transaction Multiples

When looking at the median valuations that private equity firms have been paying for Software businesses over the course of the past decade, there is clearly an upwards trend on a revenue multiple basis (TEV / Revenue). This is indicative of the increased competition for deals in the space given the growing amount of capital that is being allocated to Software-focused strategies by private equity acquirers.

What is even more interesting is looking at the median revenue multiples paid by strategic acquirers over the same period. When compared with the valuation multiples paid by private equity acquirers, it is evident that the trend is flatter over the time period and that private equity acquirers began paying higher median multiples for Software companies beginning in 2016. This is a surprising find given that strategic acquirers are the most likely to pay the higher premiums due to their ability to realize synergies with a target company. Additionally, financial buyers like private equity firms are traditionally the most reluctant to pay premium multiples given that acquiring an asset at a discounted or reasonable valuation is one of their most important levers for achieving a strong return on investment. This further supports the observation that private equity firms have a growing appetite for Software companies and are willing to pay higher valuations to acquire them.

Source: Pitchbook.

Implications on Valuations Going Forward

A key topic to consider when looking at private equity’s increasing involvement in Software is what impact it will have on valuations going forward for Software companies. It is a general rule that private equity funds want to sell their portfolio companies at a valuation that is higher than what they acquired them for. One of the most common ways to achieve a higher valuation upon exit is to sell the asset for a higher multiple than what was paid for it. However, it is becoming more and more difficult for private equity firms to sell Software assets at higher multiples given the current trend of them already paying premium valuations when they first acquire the asset.

One strategy that many private equity firms utilize that can help mitigate paying a steep multiple for an initial investment is multiple arbitrage. This is the process of acquiring smaller complementary businesses (add-on acquisitions) at lower multiples than what was paid for the initial business (platform investment) with the hopes of selling the combined entity at a multiple similar to what was paid for the initial business. This strategy allows private equity firms to effectively take the revenue or earnings of smaller assets and trade them at the higher valuation multiples of the platform asset. It is almost certain we will continue to see a rise in the number of add-on acquisitions, as well as the valuations paid for them, given the higher valuations that are being paid for platform investments by private equity firms.

An important question is what will happen to private equity-driven Software valuations if a downturn occurs in the market? Since private equity firms are all looking to exit their investments at some point, the increased number of private equity-owned Software companies would result in a market oversupply in a downturn. A rush to liquidate assets from portfolios would result in a possible catalyst that could drive valuations down even faster in a market correction scenario. That being said, if favourable market conditions persist, private equity’s growing presence in Software will continue to drive valuations higher through increased capital deployment and add-on acquisitions.

By Allen Fu of Sampford Advisors.

About Sampford Advisors

Sampford Advisors is a boutique investment bank exclusively focused on mid-market mergers and acquisitions (M&A) for technology, media and telecom (TMT) companies. We have offices in Toronto, Ottawa and the US and have done more mid-market tech M&A transactions than any other adviser