Why Canadian VC Investment Lags the US

Given our recent post on LinkedIn about the breakdown of VC investment by Canadian city attracted over 4,000 views and a lot of comments, we thought it would be worthwhile to do a deeper dive on this topic in a two-part blog post. Firstly, in this post we will examine the differences between the US and Canadian VC markets and in the second part of the blog to come in a few weeks, we will look at how VC funds are flowing by Canadian geography.

There’s no question that the VC environment in the US is significantly more active than it is here in Canada, as can be seen on the following two charts looking at overall VC investment in technology companies and the number of transactions.

Figure 1: 2016 VC Tech Investment *

A natural observation on these charts is that the US is a much bigger economy than Canada and therefore there is always going to be a gap. So, in this context we wanted to look at how much larger the US is both in terms of GDP and population.

Figure 2: GDP and Population Comparison **

When we adjust for GDP and Population we notice that the US market is still much more active than Canada’s with the biggest delta being on the total proceeds raised which is over triple the difference of the GDP multiple. The number of deals is still higher when adjusted on a GDP basis – at about 40% higher.

That leads us to our next question, why are the deal proceeds so much higher than the comparison to the number of deals? Most people would suggest that US rounds are bigger and therefore this accounts for the majority of the difference. But as you can see from the following chart, the US deals are larger but not significantly…

Figure 3: Median Deal Size ($Mn) *

When we drill down into the data further, a large part of the difference is the amount of late stage VC funding that is going into the US system vs Canada. Late Stage VC funding on a $ volume basis accounted for a whooping 58.6% of US VC funding versus Canada’s 46.7%. The chart below shows this more clearly…

Figure 4: % of Proceeds by Stage *

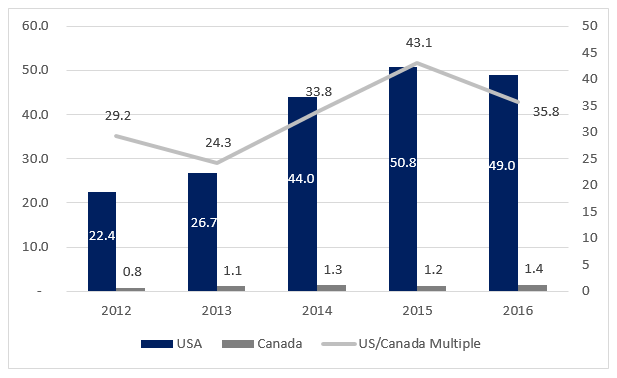

To explain it all in a nutshell, it seems that while deal sizes are slightly bigger in the US and there’s more deals happening on a per capita or GDP adjusted basis, a large part of the difference is also the amount of late stage funding that is taking place in the US. So, the last question we pose to ourselves is whether this is getting better or if the gap is widening – and unfortunately as the chart below shows, the gap has widened the last few years with a mild reversal of this trend in 2016.

Figure 5: VC Tech Investment over Time ($Bn) *

Let’s hope 2016’s gap tightening can continue in 2017 and beyond…

About the author

Ed Bryant is the President and CEO of Sampford Advisors. Ed started Sampford because he wanted to provide world-class M&A advisory services to Canadian technology companies. Ed has over 20 years of experience including over 17 years in Investment Banking with Deutsche Bank, Morgan Stanley and Sampford in Hong Kong, Singapore, New York and now Ottawa. In that time, Ed has raised in excess of $20 billion in equity and debt capital and completed over $10 billion in M&A transactions.

Visit us at www.sampfordadvisors.com.

* Source: Pitchbook. ** Source: Wikipedia.

Image Copyright: http://www.123rf.com/profile_stefanphoto