Earnings Growth Slowing Dramatically at Large Cap Tech

Given that the second quarter earnings season is largely behind us, we wanted to take a look at how the largest technology companies performed this quarter.

If you look at the technology companies within the S&P500 (there’s 91 in total), earnings growth over the last couple of quarters has slowed dramatically. This can be seen in the following chart where growth has slowed from 27% year-over-year in the third quarter of 2018 to the current pace of 1.3%.

Source: S&P CapIQ.

While a move like this might not be too concerning on its own, because of typical quarterly fluctuations, it is very concerning to us to watch the trajectory downwards over the last four quarters. So it definitely appears that the benefit from the Trump tax cuts is waning and things like the current trade war with China and overall economic uncertainty are beginning to take their toll on tech companies.

How did this all line up with analyst expectations? Well another common metric we follow is what percentage of the companies are missing expectations in a given quarter. As you can see from the chart below, after declining last quarter to 7.7%, it has risen again to 14.3%. However, this metric is a little more volatile as analysts likely paired their estimates in the first quarter after increasing 4Q18 misses. But the general upwards trend is definitely a concern.

Source: S&P CapiIQ.

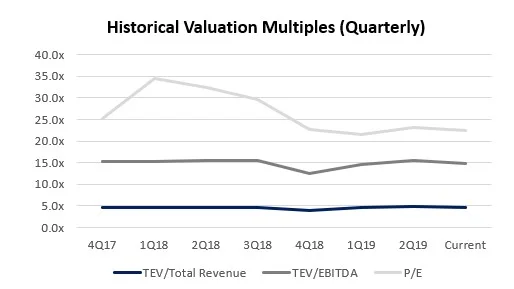

However, to really be able to extrapolate whether or not to be concerned about this, we need to think about this in the context of how these stocks are valued. If this growth rate slow-down has resulted in a re-valuation of the stocks, it might not be too much of a concern, if not, then is some sort of price correction coming? The chart below shows how these stocks have been valued for the past few quarters and as you can see, there hasn’t been any significant multiple correction for the group as a whole.

Source: S&P CapIQ.

In fact, TEV/Revenue, TEV/EBITDA and P/E multiples have remained relatively consistent. And if anything, they remain at elevated levels when you look at them since 2010. For example and as the chart below shows, the Revenue Multiple has increased from 2.4x in 2010 to 4.6x currently and over the same time period P/E has increased from 16.8x to 22.4x.

Source: S&P CapIQ.

So in the context on valuations, the lack of growth so far this year is really a concern for us as that is typically what typically drives valuation multiples of the kind that are prevalent in today’s marketplace.

About Sampford Advisors

Sampford Advisors is a boutique investment bank exclusively focused on mid-market mergers and acquisitions (M&A) for technology, media and telecom companies. We have offices in Toronto, Ottawa and the US and have done more mid-market tech M&A transactions than any other adviser.